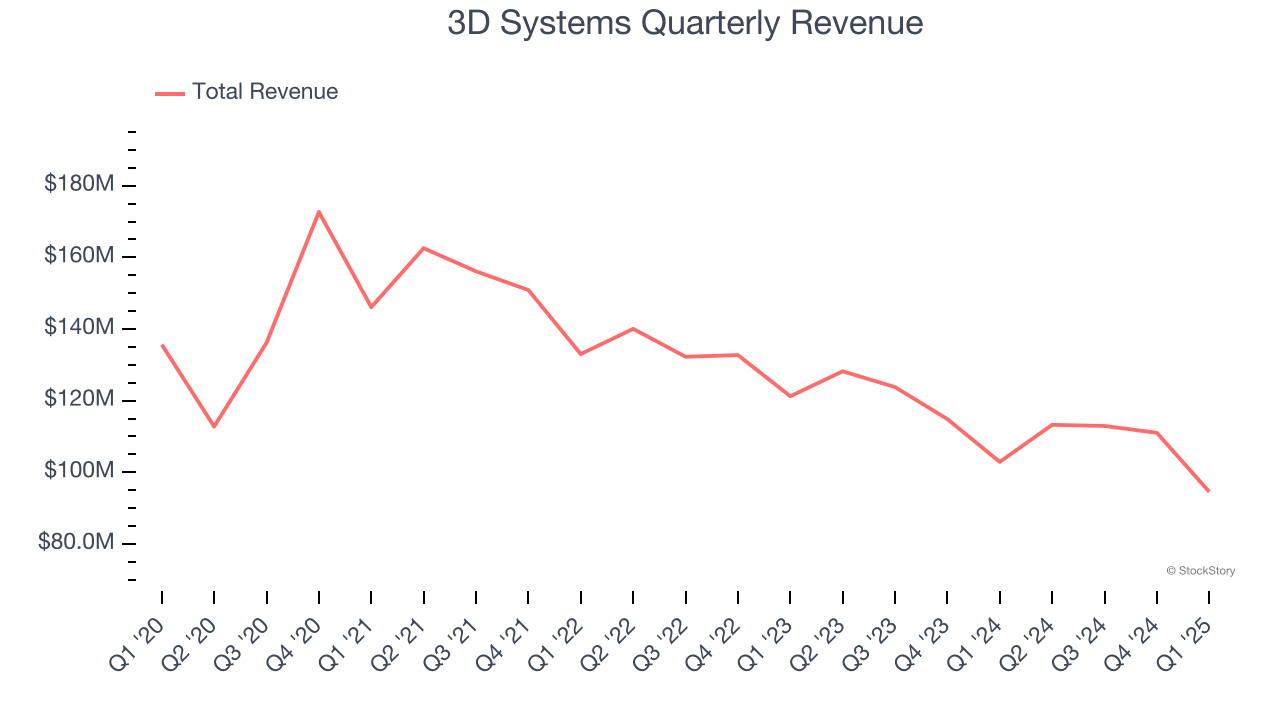

3D printing company 3D Systems (NYSE:DDD) missed Wall Street’s revenue expectations in Q1 CY2025, with sales falling 8.1% year on year to $94.54 million. Its non-GAAP loss of $0.21 per share was 44.8% below analysts’ consensus estimates.

Is now the time to buy 3D Systems? Find out by accessing our full research report, it’s free.

3D Systems (DDD) Q1 CY2025 Highlights:

- Revenue: $94.54 million vs analyst estimates of $98.31 million (8.1% year-on-year decline, 3.8% miss)

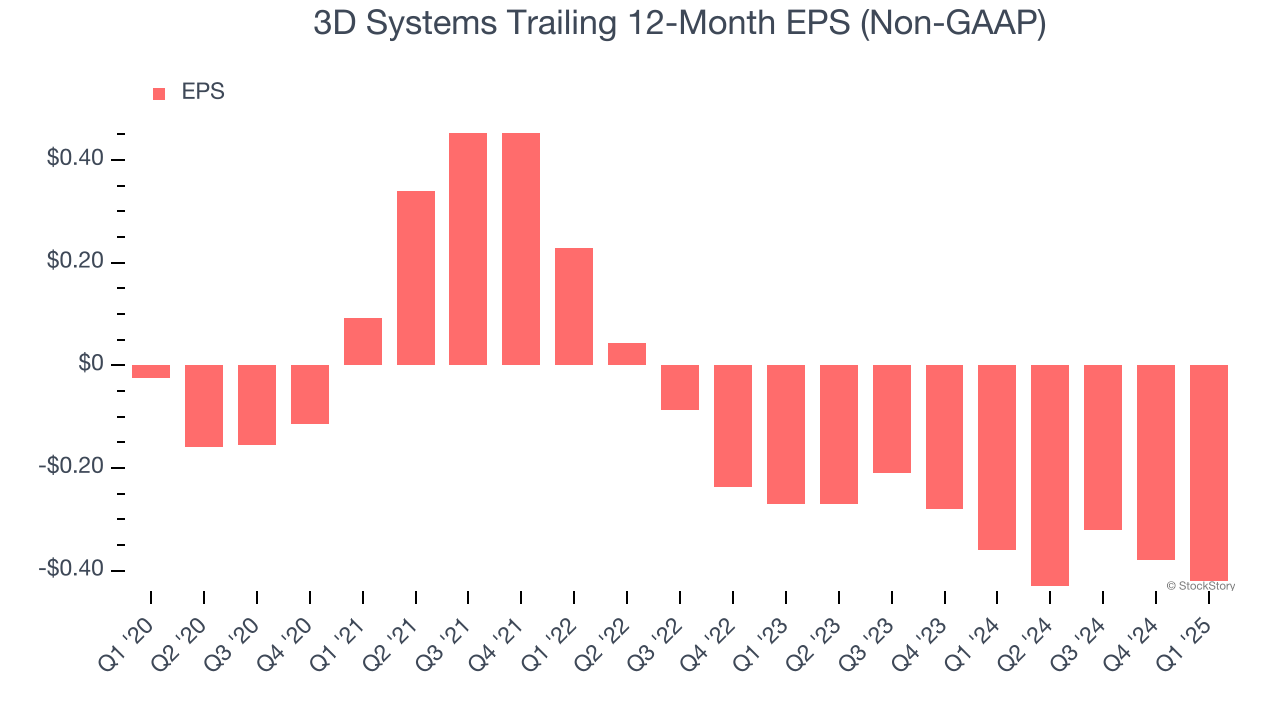

- Adjusted EPS: -$0.21 vs analyst expectations of -$0.15 (44.8% miss)

- Adjusted EBITDA: -$23.9 million vs analyst estimates of -$12.36 million (-25.3% margin, 93.3% miss)

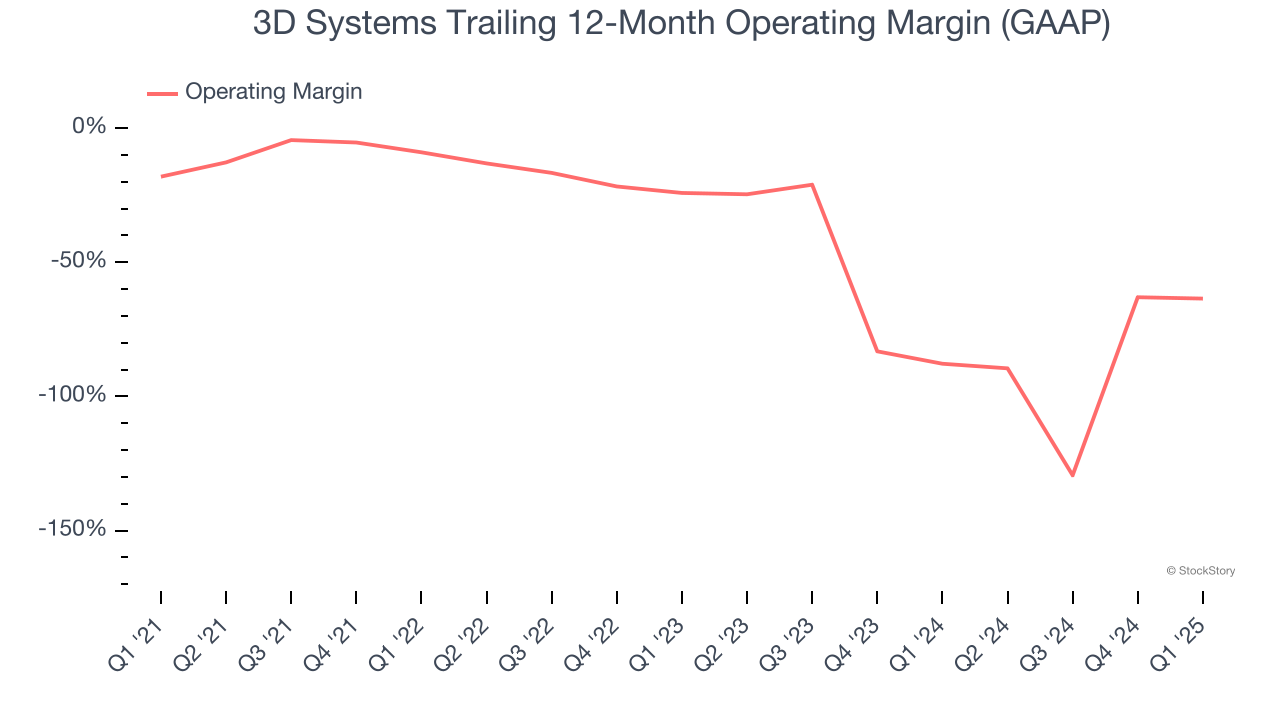

- Operating Margin: -38.9%, in line with the same quarter last year

- Free Cash Flow was -$36.58 million compared to -$28.74 million in the same quarter last year

- Market Capitalization: $321.2 million

Dr. Jeffrey Graves, president and CEO of 3D Systems said, “Our first quarter revenues reflect a continuation of challenging top-line pressures as many customers are delaying their capital investments in order to get greater clarity around potential tariff impacts on their manufacturing and distribution strategies. This is in addition to the ongoing geopolitical and broader macroeconomic uncertainty that we have been experiencing for some time. We believe that these factors led to a noticeable dampening of our customers’ near-term capital spending, particularly in consumer-facing and service bureau related end markets. While we were pleased to see this growth in new printer sales for the second straight quarter, the rate was clearly impacted by these capital spending delays. Encouragingly, this growth in printer sales was driven predominantly by our newest hardware systems, as our strengthened technology portfolio delivered strategic wins for all three of our metal printing platforms, and steady growth broadly in Aerospace and Defense markets. These wins bode well for the future, particularly in the high-reliability Healthcare and Industrial markets, which include Aerospace and Defense, and AI infrastructure, areas that have been an increasing focus for us for some time. These trends were true not only in our US markets, but also in Europe, Asia and the Middle East. With regard to materials sales, the decline we experienced was primarily related to short-term inventory management in the dental orthodontics market. More broadly within our Healthcare segment, we delivered impressive results in spite of the broader economy, with 17% growth in our Personalized Healthcare business, and 18% in our manufacturing operations for FDA-approved parts – both crucial elements of our growth strategy moving forward.”

Company Overview

Founded by the inventor of stereolithography, 3D Systems (NYSE:DDD) engineers, manufactures, and sells 3D printers and other related products to the aerospace, automotive, healthcare, and consumer goods industries.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. 3D Systems struggled to consistently generate demand over the last five years as its sales dropped at a 6.9% annual rate. This wasn’t a great result and suggests it’s a low quality business.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. 3D Systems’s recent performance shows its demand remained suppressed as its revenue has declined by 9.4% annually over the last two years.

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Industrial and Healthcare, which are 56.3% and 43.7% of revenue. Over the last two years, 3D Systems’s Industrial revenue (aerospace, defense, and transportation manufacturing) averaged 6.1% year-on-year declines while its Healthcare revenue (dental and medical devices) averaged 12.6% declines.

This quarter, 3D Systems missed Wall Street’s estimates and reported a rather uninspiring 8.1% year-on-year revenue decline, generating $94.54 million of revenue.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection indicates its newer products and services will fuel better top-line performance, it is still below average for the sector.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

3D Systems’s high expenses have contributed to an average operating margin of negative 37.4% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, 3D Systems’s operating margin decreased by 45.4 percentage points over the last five years. 3D Systems’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, 3D Systems generated a negative 38.9% operating margin. The company's consistent lack of profits raise a flag.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

3D Systems’s earnings losses deepened over the last five years as its EPS dropped 76.1% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, 3D Systems’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For 3D Systems, its two-year annual EPS declines of 24.7% show it’s still underperforming. These results were bad no matter how you slice the data.

In Q1, 3D Systems reported EPS at negative $0.21, down from negative $0.17 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast 3D Systems’s full-year EPS of negative $0.42 will reach break even.

Key Takeaways from 3D Systems’s Q1 Results

We struggled to find many positives in these results as its revenue, EPS, and EBITDA missed Wall Street’s estimates significantly. Overall, this was a weaker quarter. The stock traded down 22.9% to $1.99 immediately after reporting.

3D Systems underperformed this quarter, but does that create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.