News Source: Optimal Blue

Optimal Blue's April 2025 Market Advantage data report shows stronger purchase activity, a shifting loan mix, and signs of investor caution

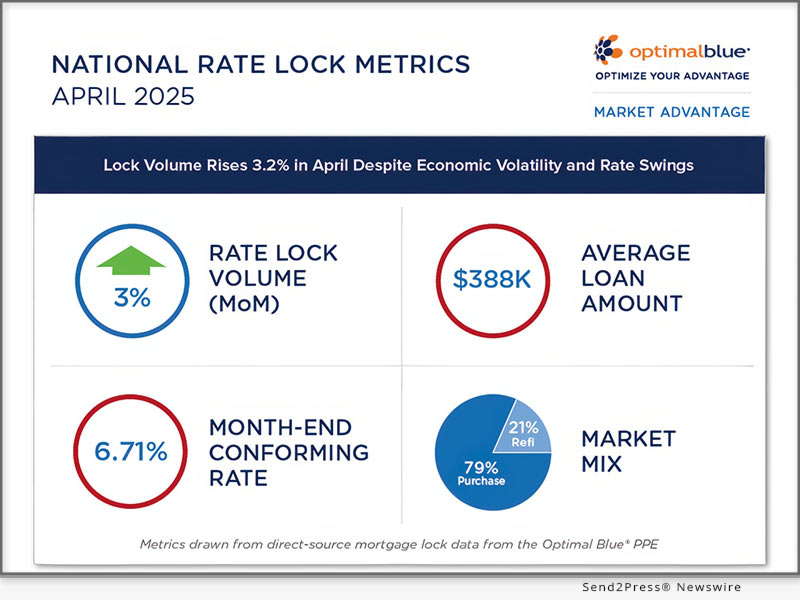

PLANO, Texas, May 13, 2025 (SEND2PRESS NEWSWIRE) — Optimal Blue today released its April 2025 Market Advantage mortgage data report showing total loan lock volume rose 3.2% month-over-month (MoM) as the spring homebuying season progressed, with purchase locks up 7.5% despite ongoing economic pressures.

Image caption: Optimal Blue’s April 2025 Market Advantage mortgage data report.

April kicked off with significant volatility in the bond market as investors responded to tariff announcements. Over the first 10 days of the month, interest rates fluctuated between 6.48% and 6.98%, a 50-basis-point (bps) range. The benchmark OBMMI 30-year conforming fixed rate briefly fell below 6.5% for the first time since October 2024 before climbing to end the month at 6.7%, about 10 bps above where it started.

“Last month’s report showed early signs of spring homebuyer activity, and April confirms the season is underway with a solid increase in purchase locks,” said Brennan O’Connell, director of data solutions at Optimal Blue. “We also saw a shift toward FHA loans, often used by first-time or credit-challenged buyers, and away from non-conforming products, possibly reflecting investor caution in response to broader economic uncertainty.”

Key findings from the Market Advantage report, derived from direct-source mortgage lock data, include:

- Interest rate turbulence: Rates whipsawed at the start of the month amid market reactions to new tariff developments, dropping by one-eighth essentially overnight. The OBMMI 30-year conforming fixed rate – the benchmark for the CME Mortgage Rate futures contract – finished April at roughly 6.7%, up from 6.6% in March. FHA rates rose 17 bps to 6.44%, VA rates rose 9 bps to 6.28%, and jumbo rates climbed 11 bps to 6.84%.

- YoY purchase volume down, again: While MoM purchase locks were up 7.5%, they were down 5% YoY. Isolating purchase loan counts reveals a deeper 7% YoY decline, continuing a trend seen each month so far this year.

- FHA loans gain ground as other categories slip: FHA share rose to 20.2% in April, gaining 50 bps, while non-agency lending fell 46 bps to 16.4%. The shift suggests reduced investor risk tolerance amid economic uncertainty. Conforming loan share dipped slightly to 51%, and VA share also declined modestly to 11.8%. USDA volume remained steady at 0.6%.

- Adjustable-rate mortgages rise: ARMs accounted for 10.34% of total lock volume in April, up from just under 9% in March, as buyers looked for ways to improve affordability.

- Refinance activity stalls: After a couple of very strong days early in the month, refinance volume fell off in response to rising interest rates. Rate-and-term refis dropped 15% MoM, and cash-out refis dipped 3%. Refinance share fell from 25% in March to 21% in April.

- Loan amounts, home prices edge down: The average loan amount declined to $387.5K from $391.7K, while the average purchase price slipped to $483.5K from $486.9K. Regional differences remain stark; average loan amounts ranged from $601,660 in the New York City metro area to $374,945 in greater Minneapolis.

The full Market Advantage report, which provides more detailed findings and additional insights into U.S. mortgage market trends, can be viewed at (PDF): https://www2.optimalblue.com/OB_MarketAdvantage_MortgageDataReport_Apr2025.pdf

This month’s Market Advantage podcast features Optimal Blue Chief Product Officer Erin Wester, discussing the impact of technological innovations in the mortgage industry. Watch or listen to the episode: https://market-advantage.captivate.fm/episode/episode-8/.

About the Market Advantage Report

Optimal Blue issues the Market Advantage mortgage data report each month to provide early insight into U.S. mortgage trends. Leveraging lender rate lock data from the Optimal Blue PPE – the mortgage industry’s most widely used product, pricing, and eligibility engine – the Market Advantage provides a view of early-stage origination activity. Unlike self-reported survey data, mortgage lock data is direct-source data that accurately reflects the in-process loans in lenders’ pipelines.

Nothing herein shall be construed as, nor is Optimal Blue providing, any legal, trading, hedging, or financial advice.

About Optimal Blue

Optimal Blue effectively bridges the primary and secondary mortgage markets to deliver the industry’s only end-to-end capital markets platform. The company helps lenders of all sizes and scopes maximize profitability and operate efficiently so they can help American borrowers achieve the dream of homeownership. Through innovative technology, a network of interconnectivity, rich data insights, and expertise gathered over more than 20 years, Optimal Blue is an experienced partner that, in any market environment, allows lenders to optimize their advantage from pricing accuracy to margin protection, and every step in between. To learn more, visit https://OptimalBlue.com/.

MULTIMEDIA:

Image link for media: https://www.Send2Press.com/300dpi/25-0513-s2p-opbluapril-300dpi.jpg

{kind=link}

Image caption: Optimal Blue’s April 2025 Market Advantage mortgage data report.

This press release was issued on behalf of the news source (Optimal Blue), who is solely responsible for its accuracy, by Send2Press Newswire.

To view the original story, visit: https://www.send2press.com/wire/lock-volume-rises-3-2-in-april-driven-by-uptick-in-fha-loans-despite-economic-volatility/

Copr. © 2025 Send2Press® Newswire, Calif., USA. -- REF: S2P STORY ID: S2P126135 FCN24-3B

INFORMATION BELOW THIS PAGE, IF ANY, IS UNRELATED TO THIS PRESS RELEASE.